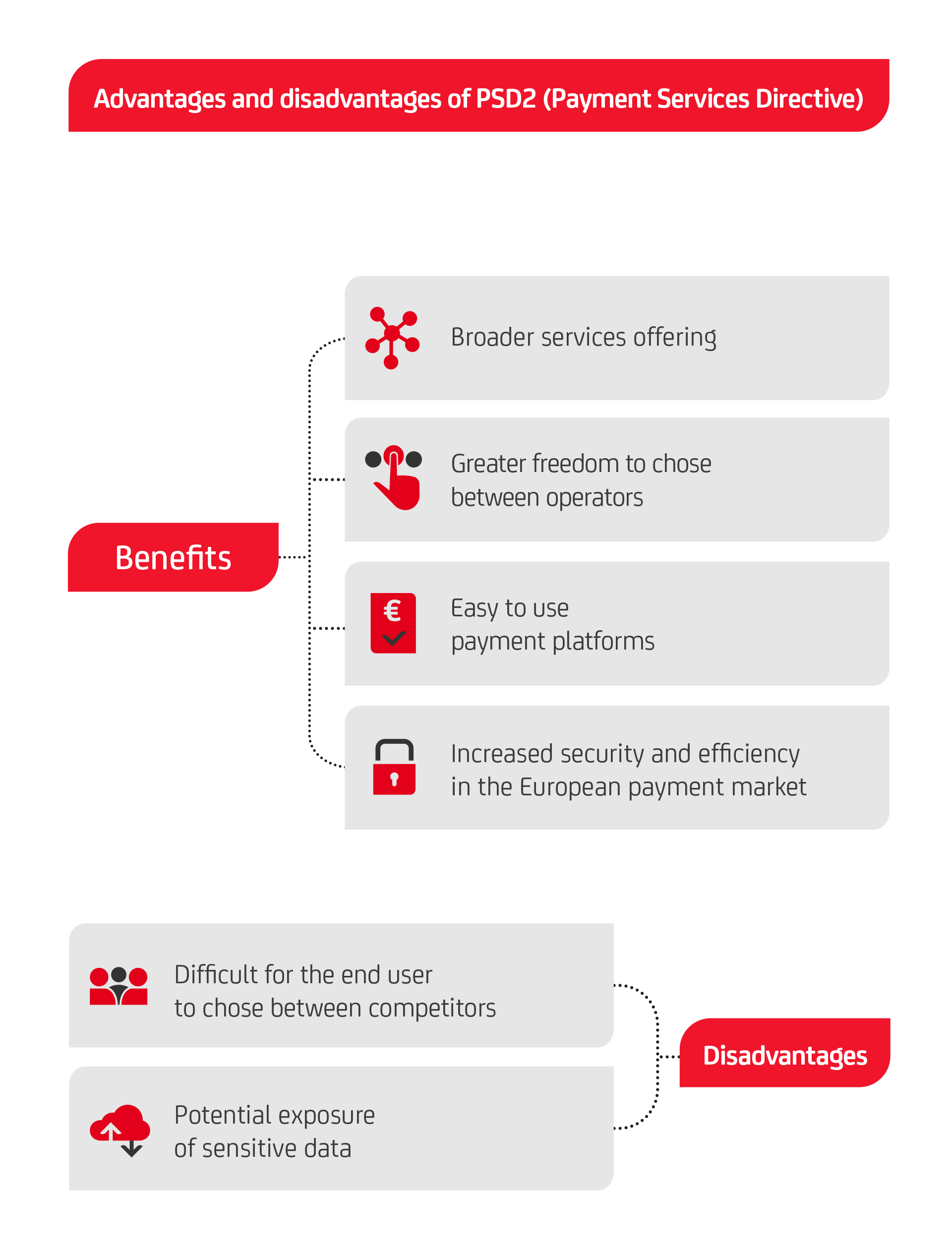

This new EU directive is broadening the horizons of online payment and banking services and will make life easier for millions of consumers.

More versatile, convenient and secure digital payments. The new PSD2 regulation issued by the European Union, which took effect in Italy on 13 January 2018, is revolutionising the digital economy world and consequently the habits of millions of European consumers. Let’s take a closer look.

PSD2 is the acronym for Payment Services Directive 2. With this legislation, which is a significant step forward from its predecessor PSD, the European Parliament intended to create an even more integrated payment system, supporting technological innovation and increasing the security level of digital payments.

One of the main aims of PSD2 is to increase transparency for the sector’s service providers and users, standardising the rights and obligations connected with individual payment services. The other aim is to increase competition between old and new players in national payment markets, while ensuring a level playing field.

In practice, PSD2 requires banks to "open the doors" to let regulator-approved third parties view customer accounts and data, subject to customer authorisation, using technological solutions such as banking APIs to interface with each other.

This new regulation paves the way for Open Banking by allowing new Third-Party Payment Services Providers (or TPPs) to enter the payment ecosystem, offering new services and innovative user-centred products.

With Open Banking, apps and dashboards will be available that will allow users to manage different current accounts in a single, easy-to-use interface. PSD2 introduces another important innovation: the use of telephone credit (prepaid or included on your bill) for payment transactions in addition to those already available (digital content, donations or electronic tickets).

When it comes to security and authentication, PSD2 introduces the concept of 'Strong Customer Authentication' (SCA) to identify and authenticate the customer with two recognition components (for example a numeric pin and a biometric component) obliging the payment service provider to apply it when the payer accesses his payment account online or has an electronic payment transaction. The technical regulatory standards for these security systems, drawn up by the European Banking Authority (EBA), were issued by the European Commission and took effect on 14 September 2019.

Finally, PSD2 deals with online scams and careless digital payments by offering greater protection to consumers.

Customers will be charged a maximum of €50 for any unauthorized payment, compared to €150 in the previous PSD.

This consumer protection is combined with rules in EU regulation 2015/751, which says e-commerce surcharges cannot be applied for consumer debit and prepaid transactions (excluding cards issued for business or public administration purposes).

PSD2 is still in the initial stages, but the system has the potential to change the way we make payments and more generally benefit the banking sector.